PayPal's Revenue Continues to Climb. But 1 Important Metric Is Still Trending in the Wrong Direction

PayPal Holdings (NASDAQ: PYPL) is a financial-technology (fintech) pioneer that's still extremely relevant. As of the first quarter of 2024, the company had 427 million active accounts. And its system processed over $400 billion in payments during Q1 alone. That's a big platform that's still getting plenty of use.

As of this writing, PayPal stock is down nearly 80% from its all-time high and about 14% over the past year. Based on this stock performance, one might conclude that business is poor. But to the contrary, the company's revenue and total payment volume are currently at all-time highs.

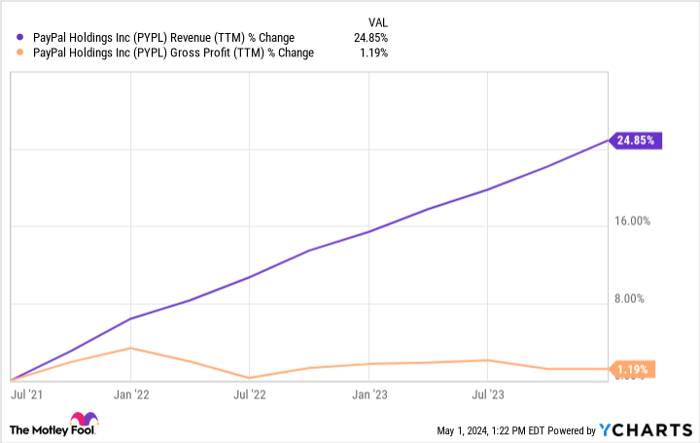

However, there is one chart that might explain PayPal's current situation better than any other. As the chart below shows, the company's revenue is up 25% over the past three years, which isn't bad at all. However, its gross profit is flat over this same time frame.

PYPL Revenue (TTM) data by YCharts. TTM = trailing 12 months.

Therefore, PayPal has grown its business in recent years, which is exactly what investors want to see. However, profit-wise, this growth has been a complete wash, which is troubling.

Here's why PayPal's growth hasn't moved the needle at all in recent years.

Was this the right strategy for PayPal?

Before PayPal was a publicly traded company, it acquired a fintech company called Braintree for $800 million. Braintree is the behind-the-scenes pipes that many businesses use to receive digital payments. The service is unbranded, meaning there's no PayPal logo slapped anywhere on the page. Therefore, investors could have used PayPal's Braintree without realizing it.

Braintree has gained serious momentum in recent years for PayPal. In Q1, the company's unbranded checkout payment volume (mostly Braintree) was up 26% year over year (adjusting for fluctuations in currency exchange rates). Therefore, Braintree was the biggest driver of PayPal's payment-volume growth.

Moreover, PayPal's unbranded payment volume now accounts for 37% of its total payment volume. For perspective, unbranded volume made up just 24% of its total payment volume as recently as 2022. These services are clearly catching on and driving payment-volume growth for PayPal.

However, this growth has come at a cost. In Q1, PayPal had a transaction margin of 45%. For perspective, the company had a transaction margin of 58% in the same quarter of 2021. Therefore, the inference is simple: As Braintree has grown in importance, PayPal's margins have suffered.

This was acknowledged by PayPal's new CEO, Alex Chriss. At the Morgan Stanley Technology, Media & Telecom Conference, Chriss said that Braintree was "Really priced aggressively in order to gain customers over the last few years."

In other words, PayPal has priced its Braintree services really low to gain market share. This has accomplished its purposes of gaining share and growing volume. But from a profitability standout, it's kept the company from making any progress in recent years.

A change in strategy on the horizon

Chriss has been PayPal's CEO for about six months. And he's indicated a change of strategy is in the works. Whereas prior management priced Braintree services low to gain market share, Chriss said he's looking to implement a price-to-value strategy -- this approach aims to charge the maximum price customers are willing to pay.

According to management, PayPal's built a great product, and its customers should, consequently, be willing to pay more to use it. If true, the company could be on the verge of reinvigorating profit margins. That could go a long way in reversing the negative trend in the chart below.

PYPL Revenue (TTM) data by YCharts. TTM = trailing 12 months.

However, PayPal's investors must take this with a grain of salt before getting too excited. The company has essentially positioned itself in the market as a low-cost leader. Transitioning from this to more premium pricing might not happen without substantial pushback from customers. And in the fintech space, there are plenty of other options for PayPal's customers to choose from.

Simply put, PayPal will be navigating a delicate situation in 2024. Chriss has a background in working with small and medium-sized businesses, so he's encouragingly a good leader for the job. But investors might want to give this a few quarters to play out before determining whether the impact will be positive or negative for the business.Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for two decades, Motley Fool Stock Advisor, has more than tripled the market.*

They just revealed what they believe are the 10 best stocks for investors to buy right now… and PayPal made the list -- but there are 9 other stocks you may be overlooking.

See the 10 stocks

*Stock Advisor returns as of April 30, 2024Jon Quast has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends PayPal. The Motley Fool recommends the following options: short June 2024 $67.50 calls on PayPal. The Motley Fool has a disclosure policy.

Welcome to Billionaire Club Co LLC, your gateway to a brand-new social media experience! Sign up today and dive into over 10,000 fresh daily articles and videos curated just for your enjoyment. Enjoy the ad free experience, unlimited content interactions, and get that coveted blue check verification—all for just $1 a month!

Account Frozen

Your account is frozen. You can still view content but cannot interact with it.

Please go to your settings to update your account status.

Open Profile Settings