Is Sending Crypto to Another Wallet Taxable?

Yes, sending crypto to another wallet can be taxable, depending on the nature of the transaction and the jurisdiction you reside in.

Cryptocurrency transactions are increasingly under the scrutiny of tax authorities worldwide. Understanding the tax implications of sending crypto from one wallet to another is crucial to avoid potential legal issues and ensure compliance.

Key highlights:

Sending crypto to another wallet can trigger tax events.

The nature of the transaction determines taxability.

Record-keeping is essential for tax reporting.

Consulting a tax professional is advisable for complex transactions.

Tax laws vary by jurisdiction and are subject to change.

Is sending crypto to another wallet taxable?

Yes, sending crypto to another wallet can be taxable. The tax implications vary based on factors such as whether the transfer involves a sale, a purchase, or a gift, and your country’s tax regulations. In many jurisdictions, cryptocurrency is treated as property for tax purposes, meaning that any transaction can potentially trigger a taxable event.

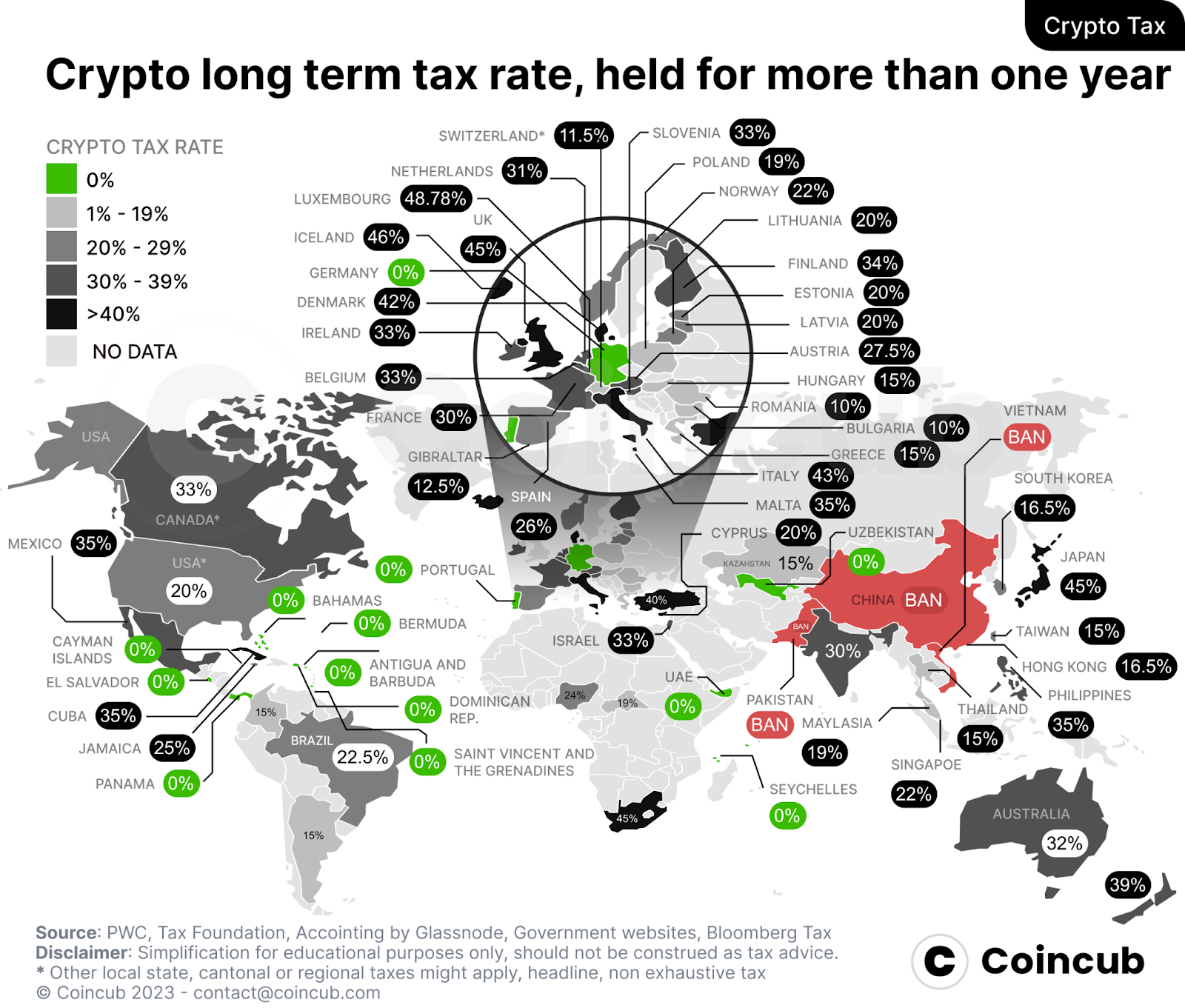

There are several distinctly crypto-friendly countries where there is no tax on transactions or long-term holding. Image source: Coincub

Types of transactions and their tax implications

1. Transfers between personal wallets

Generally non-taxable: If you transfer crypto between your wallets without selling or buying, it's usually non-taxable. However, keep detailed records of these transactions. This is because, while the transaction itself might not be taxable, proving that no taxable event occurred can save you from potential issues in the future.

Record-keeping: Maintain records of the transfer to prove it's a non-taxable event. This includes the date of the transaction, the value of the cryptocurrency at the time of transfer, and any associated transaction fees.

2. Gifts

Gifting crypto: Sending crypto as a gift can have different tax implications based on your jurisdiction. In some countries, gifts above a certain value may be subject to gift tax. In the US, for instance, gifts exceeding a specific annual limit ($15,000 per recipient as of 2021) may require filing a gift tax return.

Recipient's responsibility: The recipient may need to report the received crypto's value for tax purposes. If the recipient later sells the crypto, they will need to know the original purchase price (cost basis) to calculate any capital gains.

Scenario

Tax implication

Action required

Transfer to Self

Non-Taxable

Maintain records of the transfer

Gift to Another

Potentially Taxable

May need to file a gift tax return

Sale or Purchase

Taxable

Report capital gains or losses

3. Sales and purchases

Taxable events: If sending crypto involves selling it or using it to purchase goods/services, it triggers a taxable event. You need to report any capital gains or losses. For example, if you use Bitcoin to buy a car, you must report the difference between the Bitcoin's value when you acquired it and its value when you spent it.

Calculating gains/losses: Calculate the difference between the purchase price (cost basis) and the sale price to determine capital gains or losses. This calculation is essential for accurately reporting taxable income and can be complex, especially if the crypto was acquired through multiple transactions.

Transaction type

Cost basis calculation

Reporting requirement

Sale

Difference between sale and purchase price

Report as capital gain/loss

Purchase of Goods/Services

Difference between crypto value at purchase and usage

Report as taxable event

Tax reporting

Detailed records: Keep comprehensive records of all transactions, including dates, values, and purposes. Use a reliable cryptocurrency tax software to track your transactions and calculate your tax liabilities accurately.

Consult a tax professional: Tax laws for crypto are complex and vary by jurisdiction. Consult a tax professional for personalized advice. They can help you understand the nuances of the law, avoid common pitfalls, and take advantage of any applicable deductions or credits.

International considerations

Tax laws vary significantly from one country to another. In some jurisdictions, cryptocurrencies are heavily regulated, while in others, they might still be in a legal gray area. Here are a few examples:

Country

Tax treatment of crypto transactions

Key considerations

United States

Treated as property

Detailed reporting required, frequent updates in law

European Union

Varies by member state

Mixed treatment, ongoing regulatory developments

Japan

Treated as financial assets

Subject to capital gains tax, clear guidelines

China

Most crypto transactions banned

Ownership allowed but transactions restricted

If you want to dive deeper into the topic of crypto taxes in different countries, consider checking the following articles:

Crypto Taxes in the UK

Crypto Taxes in Canada

Crypto Taxes in India

Crypto Taxes in Germany

Crypto Taxes in Italy

Practical tips for managing crypto taxes

Use crypto tax software: Crypto tax software like CoinTracking, Koinly, or CryptoTrader.Tax can help you keep track of transactions and calculate your tax liabilities accurately.

Stay updated on tax laws: Cryptocurrency tax laws are evolving. Regularly check for updates from your tax authority or consult with a tax professional.

Consider professional help: Given the complexity, professional tax advice can be invaluable, especially for large or complex portfolios.

Advanced tax strategies for crypto transactions

For more sophisticated investors, there are advanced strategies to optimize tax outcomes:

Tax loss harvesting:

Definition: Selling underperforming investments at a loss to offset gains from other investments.

Benefits: Reduces taxable income and can be used to offset up to $3,000 of ordinary income per year in the U.S.

Long-term vs. Short-term gains:

Definition: Holding assets for more than one year qualifies for long-term capital gains tax rates, which are typically lower than short-term rates.

Strategy: Plan your crypto sales to maximize long-term gains where possible to benefit from reduced tax rates.

Using retirement accounts:

Crypto in retirement accounts: Some IRAs and 401(k)s allow for crypto investments, offering tax-deferred or tax-free growth.

Benefits: Reduces taxable events until retirement withdrawals.

Final words

Sending crypto to another wallet can be taxable depending on the transaction type and jurisdiction. Always keep detailed records and seek professional tax advice to ensure compliance. Understanding the nuances of crypto transactions and their tax implications can save you from potential legal issues and financial penalties. By employing effective tax strategies, you can optimize your crypto investments and minimize tax liabilities.

If you are unsure about the status of the tax code in your jurisdiction regarding to cryptocurrency transactions, we suggest you get in touch with crypto lawyers who are specialized in crypto and blockchain. Meanwhile, for filing taxes, you should strongly consider the services of top crypto tax accountants.

Welcome to Billionaire Club Co LLC, your gateway to a brand-new social media experience! Sign up today and dive into over 10,000 fresh daily articles and videos curated just for your enjoyment. Enjoy the ad free experience, unlimited content interactions, and get that coveted blue check verification—all for just $1 a month!

Account Frozen

Your account is frozen. You can still view content but cannot interact with it.

Please go to your settings to update your account status.

Open Profile Settings